Understanding Mortgage Rates: What You Need to Know

Hey there! If you're in the market for a new home or thinking about refinancing, you're probably wondering about mortgage rates. Let me break it down for you. Mortgage rates play a big role in determining how much you'll pay for your home over time. With so many options out there, it’s important to understand what affects these rates and how you can get the best deal possible. Whether you're buying a starter home or refinancing your existing property, having the right information can save you thousands of dollars.

Why Mortgage Rates Matter

Mortgage rates are more than just numbers—they’re the key to unlocking your dream home without breaking the bank. These rates determine the cost of borrowing money, so a small difference in percentage points can add up to significant savings over the life of your loan. For instance, if you’re taking out a $300,000 mortgage, even a 0.5% difference in interest rates could mean hundreds of dollars in savings each month. That’s why it’s crucial to shop around and compare rates from multiple lenders.

How to Find the Best Mortgage Rates

Let’s talk about how you can find the best mortgage rates. First, it’s important to know that rates vary depending on factors like your credit score, down payment, and the type of loan you choose. A good place to start is by using a reliable mortgage calculator to estimate your payments. From there, you can explore different loan programs and see which one fits your financial situation. Don’t hesitate to reach out to lenders directly for personalized recommendations tailored to your needs.

Read also:Charlie Ciaffa The Rising Star Breaking Barriers In The Entertainment World

Current Mortgage Rates: What’s Happening Now?

As of today, mortgage rates are hovering around 6.707%, according to data from Mortgage Data Company Optimal Blue. While rates have been fluctuating recently due to market conditions, they remain higher than they were a few years ago. This trend is largely influenced by economic factors, including inflation and Federal Reserve decisions. However, it’s worth noting that rates can change daily, so staying informed is key. Check back often to see the latest updates and make sure you’re getting the best rate possible.

Factors That Affect Mortgage Rates

Several factors come into play when determining mortgage rates. Your credit score is one of the biggest influences—lenders typically offer lower rates to borrowers with higher scores. Another important factor is the size of your down payment. The more you put down upfront, the less risky you appear to lenders, which can lead to better rates. Additionally, the location of the property and the type of loan you choose (fixed-rate, adjustable-rate, etc.) will also impact the rate you’re offered.

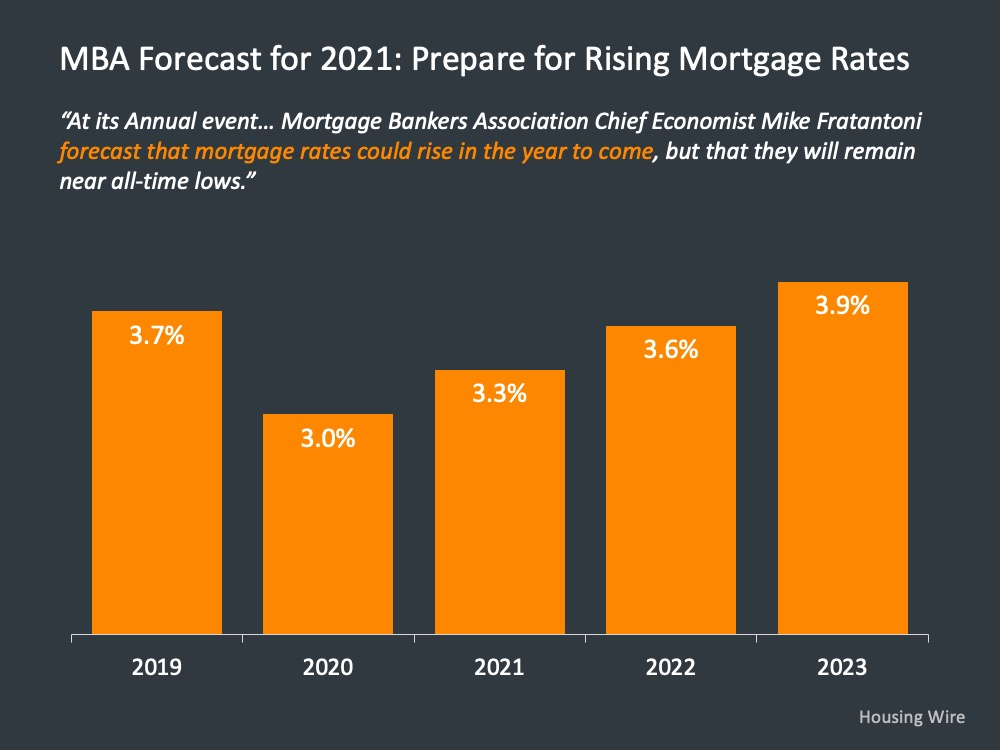

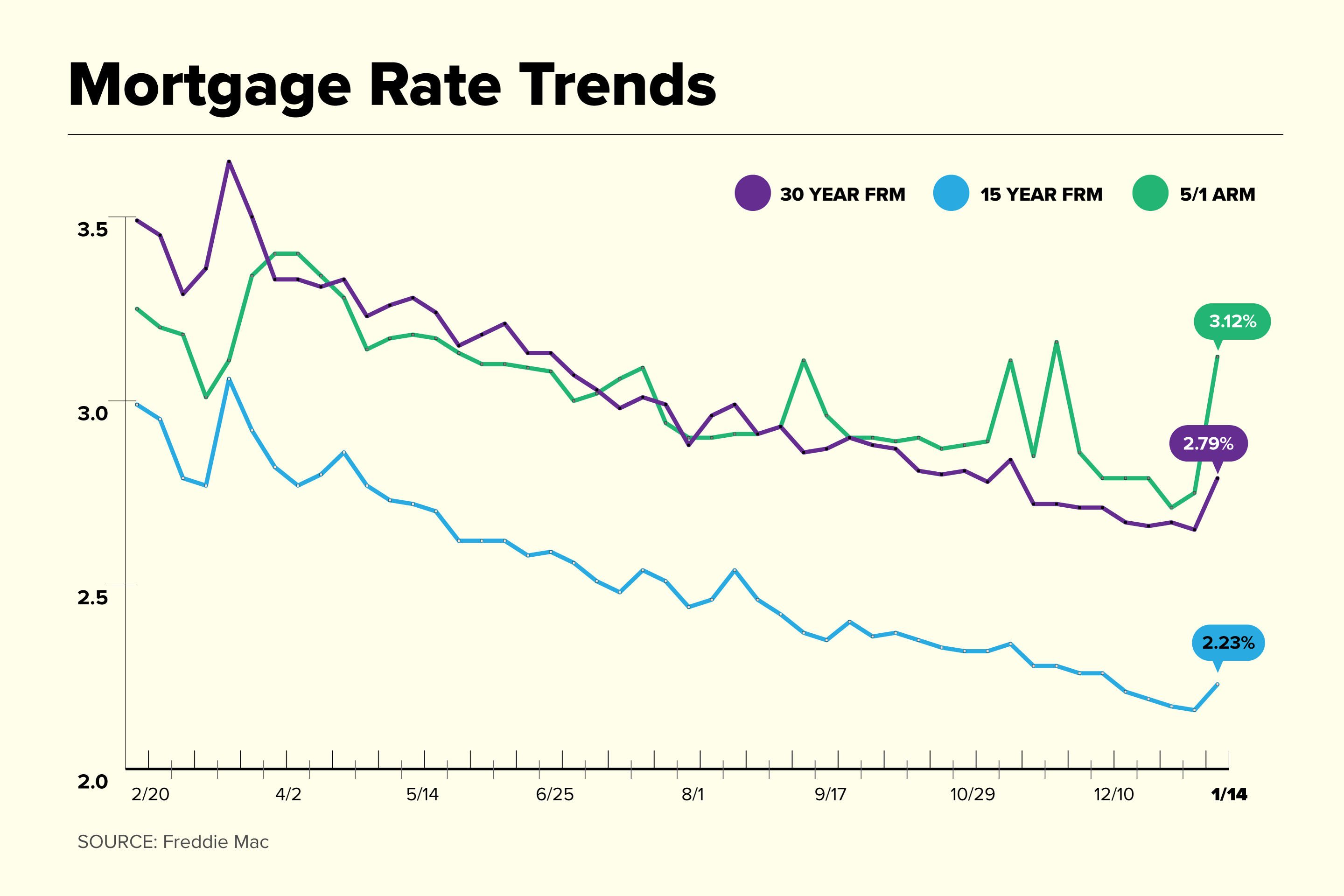

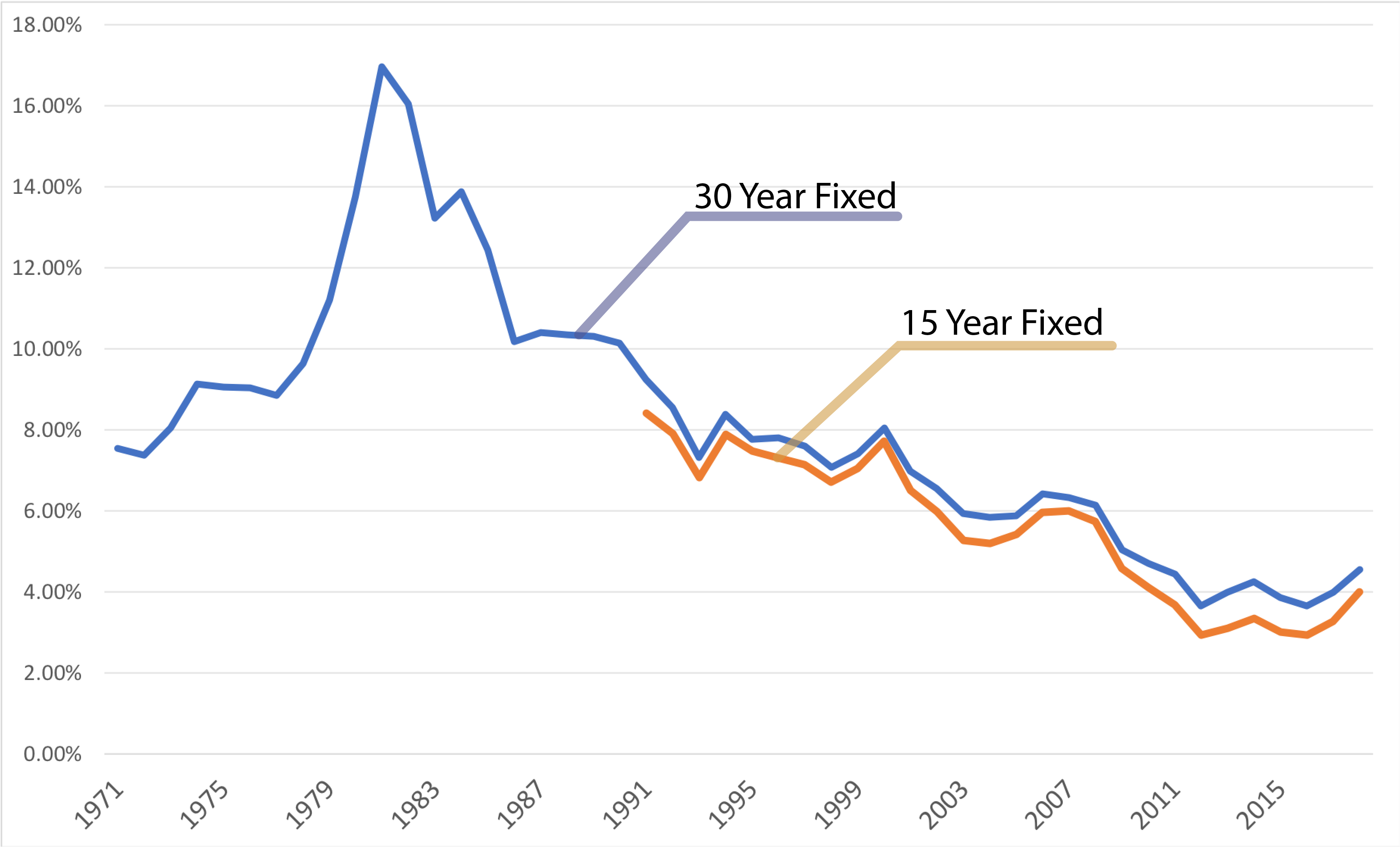

Historical Perspective on Mortgage Rates

Looking back at the history of mortgage rates can provide valuable context. Over the past few decades, rates have fluctuated significantly, often reflecting broader economic trends. Since 2019, we’ve seen some dramatic shifts in the real estate market, especially due to the pandemic. Many people reevaluated their living situations, leading to increased demand for homes and, consequently, higher mortgage rates. As we move forward, experts predict that rates will likely remain above 6% for the foreseeable future. However, if market conditions change, we could see some relief for borrowers.

Refinancing: Is It Worth It?

If you already own a home, you might be wondering whether refinancing is a good idea. The answer depends on several factors, including your current mortgage rate and the current market rates. In general, if you can secure a rate that’s at least 1 percentage point lower than your current one, refinancing could save you money in the long run. Even a smaller difference, like 0.5%, might be worth considering if it reduces your monthly payments significantly. Just remember to factor in any fees associated with refinancing to ensure it’s a financially sound decision.

How to Compare Mortgage Rates

Comparing mortgage rates might seem overwhelming, but it doesn’t have to be. Start by gathering quotes from at least three different lenders. This will give you a better sense of what’s available and help you avoid settling for a subpar rate. Pay attention to not just the interest rate but also the annual percentage rate (APR), which includes additional costs like origination fees. Once you’ve collected your quotes, take the time to review them carefully and consider which option aligns best with your long-term financial goals.

Tips for Getting the Best Mortgage Rate

Here are a few tips to help you secure the best mortgage rate possible. First, work on improving your credit score before applying for a loan. Even small improvements can make a big difference in the rates you’re offered. Second, consider making a larger down payment if it’s feasible for you. This reduces the lender’s risk and often leads to better terms. Lastly, don’t be afraid to negotiate. Lenders want your business, so if you find a better rate elsewhere, let them know—you might just get an even better offer.

Read also:Who Is Lou Ferrigno Jr Unpacking The Legacy Of A Fitness Icon

Stay Informed: Your Path to Smart Homeownership

In conclusion, understanding mortgage rates is an essential part of becoming a smart homeowner. By staying informed about current rates, knowing what factors influence them, and taking steps to improve your financial standing, you can position yourself to get the best deal possible. Whether you’re buying your first home or refinancing your existing mortgage, remember that knowledge is power. Keep checking back for the latest updates and tools to help you navigate this exciting journey.

Ready to take the next step? Get a free quote in minutes and find out how much you could borrow today. Your dream home is waiting—let’s make it happen!